Traditional on Roth?

One of the Ford-Chevy decisions in retirement planning is whether to utilize traditional tax-deductible accounts, or Roth savings accounts.

Traditional tax-deductible savings accounts:

- Pre-tax 401(k)

- Traditional IRA

Here, you contribute pre-tax dollars[1], your money grows tax-deferred, and withdrawals are taxed as current income after age 59½.

Roth savings accounts:

- Designated Roth 401(k)

- Roth IRA

Here, you contribute after-tax dollars, your money grows tax-free, and you can generally make tax-free withdrawals after age 59½.[2]

The decision of which to select is at first difficult because the two account types vary widely in participation rules, tax treatment, rules surrounding withdrawals, etc.. Let’s begin a high-level comparison with the basic investment math as seen following in the calculations for our client HairyDawg, who begins with $4,000.

Option 1: Traditional IRA

- Contributions are pre-tax so HairyDawg invests the full $4,000

- $4,000 grows tax-deferred for 20 years at an annual rate of 6%

- End value: $12,829

- All retirement withdrawals will be taxed as ordinary income

- If Hairy’s effective tax rate in retirement is 25%, Uncle Sam actually owns $3,207 of Hairy’s IRA

IRA value attributable to Hairy: $9,621

______

Option 2: Roth IRA

- Contributions are after tax, so after paying 25% in taxes, HairyDawg invests the remaining $3,000

- $3,000 grows tax-free for 20 years at an annual rate of 6%

- End value: $9,621

- All retirement withdrawals are tax-free

IRA value attributable to Hairy: $9,621

These identical calculations leave us with a “six or one-half dozen” perspective and fail to provide much in the way of guidance. Thus, we must continue our analysis to determine which is better.

One time-tested approach has been to look to marginal tax rates for federal income tax to make the selection:

- Lower two federal tax brackets (10-12%) -> choose Roth

- Middle tax brackets (22-24%) -> choose Roth and/or Traditional

- Highest three tax brackets (32-37%) -> choose Traditional[3]

The working assumption here is that earners subject to high income tax brackets are likely to benefit from lower tax brackets in retirement as their income declines.[4] This basic guide would advise that a high-income earner shun Roth options and take the tax break now.

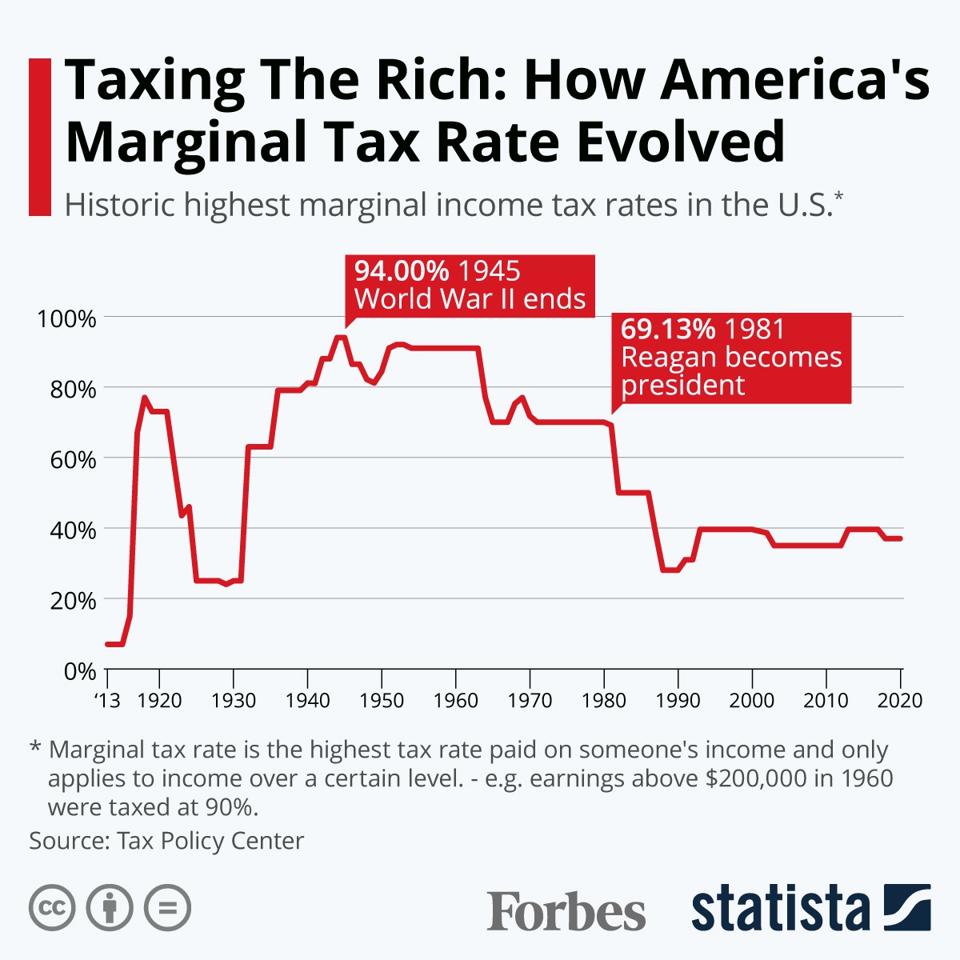

However, we must note that present tax rates are relatively low when one surveys tax policy from World War I to the present. Should taxes rates rise precipitously and they can be much higher as seen in this graphic[5], saving the tax bill for later will prove to be a mistake.

{kind=link}

There is at least a weak consensus that tax rates are likely to rise in the future, due in part to the US’ changing demographics and large debt burden. When thinking about what Uncle Sam might demand of taxpayers, consider, for example, Social Security where each “beneficiary” is now supported by only 2.8 “covered workers.” (2.8 to 1) This ratio was 16.5 to 1 in 1950.[6]

For those concerned that income tax rates are likely to rise, the Roth option may look more attractive.

There are many nuances and complicating factors that remain beyond the scope of this comparison, to include the following:

- Situational specifics that in certain cases argue strongly for one of the options

- Roth IRAs are unavailable to certain high-income earners[7]

- Roth IRAs have the advantage of no Required Minimum Distributions in retirement[8]

- Roth IRA contributions require runway and positive investment returns to recoup the immediate tax benefit of pre-tax contributions

All things considered, I am happy to rest the debate on the following proposal: splitting the difference by making both before- and after-tax retirement investments makes good financial sense for a large middle swath of retirement investors. Because predicting the future with regard to asset levels and personal income entails some level of uncertainty, and because predicting future tax policy and other relevant financial regulations entails massive uncertainty, this middle course is a low-risk, prudent strategy.

This might take different forms:

- Phased approach – young worker selects Roth investment ahead of his peak earning years, and then shifts to traditional pre-tax savings vehicles that provide an immediate tax deduction when he reaches the higher tax brackets

- 50/50 – splitting annual contributions 50/50 between pre-tax and Roth options

However implemented, by splitting contributions, the investor gains something that always carries great value – diversification. In this case, the retirement investor is making offsetting bets on tax policy and the exact shape of his future financial situation relative to the present. For the middle 60-80% of retirement savers, splitting contributions should prove a solid strategy.

[1] One can also invest after-tax dollars but this advanced strategy will not be treated here

[2] Account must be open at least five years to avoid penalties

[3] Often, it can make sense to consider a Roth Conversion(s) later

[4] Here planning is required as one must consider all future income sources: earned income during retirement years, RMDs, Social Security Retirement Payments, pension, trust and investment income, etc.

[5] In 1918, the top marginal tax rate was 77%, in 1932 it was 63%, in 1944 it peaked at 94%, and it was never below 50% at any point in the three decades spanning the 50s to the 70s.

[6] https://www.ssa.gov/history/ratios.html

[7] MFJ phase-out $204-214K for direct contributions; backdoor Roth contributions are available to those without a balance in tax-deferred IRAs such as a Traditional, SEP and/or SIMPLE IRAs

[8] Traditional IRA owners must begin taking RMDs in the year they turn 72

Recent Comments